The Use of Yield Curve Control in the United States: A Story From History

The Use of Yield Curve Control in the United States: A Story From History

I’ve read a lot of pieces this week about where the markets are heading. Based on historical patterns I’m going to discuss trends we could see occur in this current market, specifically the bond market. History never repeats, but the same trends are seen. We often see the path of a financial crisis occur in the same way. But, they all have different causes. It all comes from extremes.

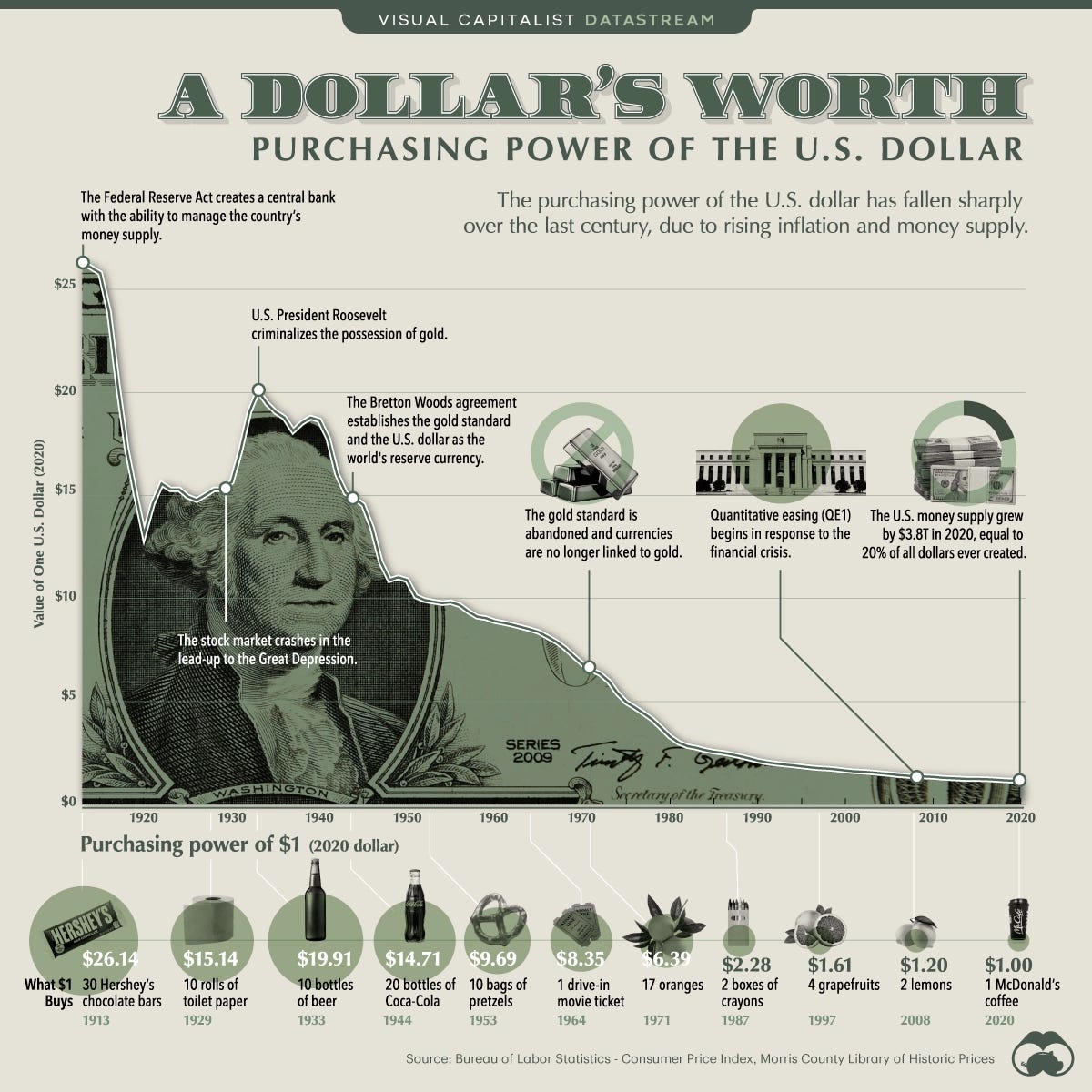

This time, the extreme was printing so much money to hand out during COVID. The US debt balance sheet expanded. When debt is used to fund expansion, there often comes a time when a currency has to be devalued.

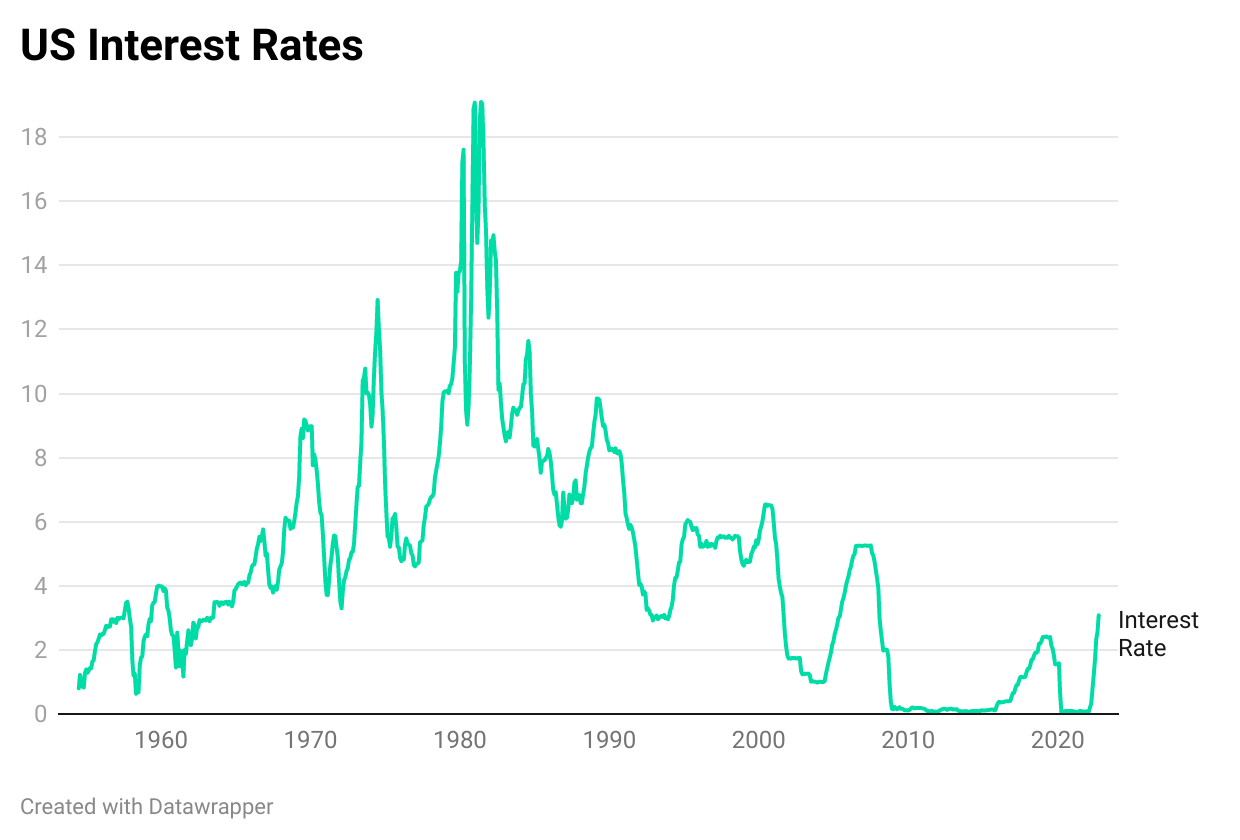

These were the underlying causes. We had unpredictable (exogenous) shocks such as the Russian invasion of Ukraine highlighting the massive energy dependency Europe had on cheap Russian energy. But when we look deeper into history there are always even more causes. It just depends on how the situation is framed. Low-interest rates since the 1980s have led to this debt-funded overinflated valuation of the stock market especially and as interest rates have risen to counter inflation, we’re only now noticing how reckless it was to push it to such extremes.

Buying of bonds is low because yields have risen due to interest rates rising. This means bond prices are low. So you get a higher yield when the bond reaches the end of its period, but the bond is worth less. Rising US interest rates mean nobody wants to buy US debt because it suggests yields will continue to rise and prices will continue to fall.

Think of the US bond market as US debt. They use it to fund expansion and spending. That’s why they are selling bonds, called quantitative tightening, in an attempt to reduce expansion and spending, which in turn should work to reduce the amount of US debt and bring down inflation. But it’s not a quick process.

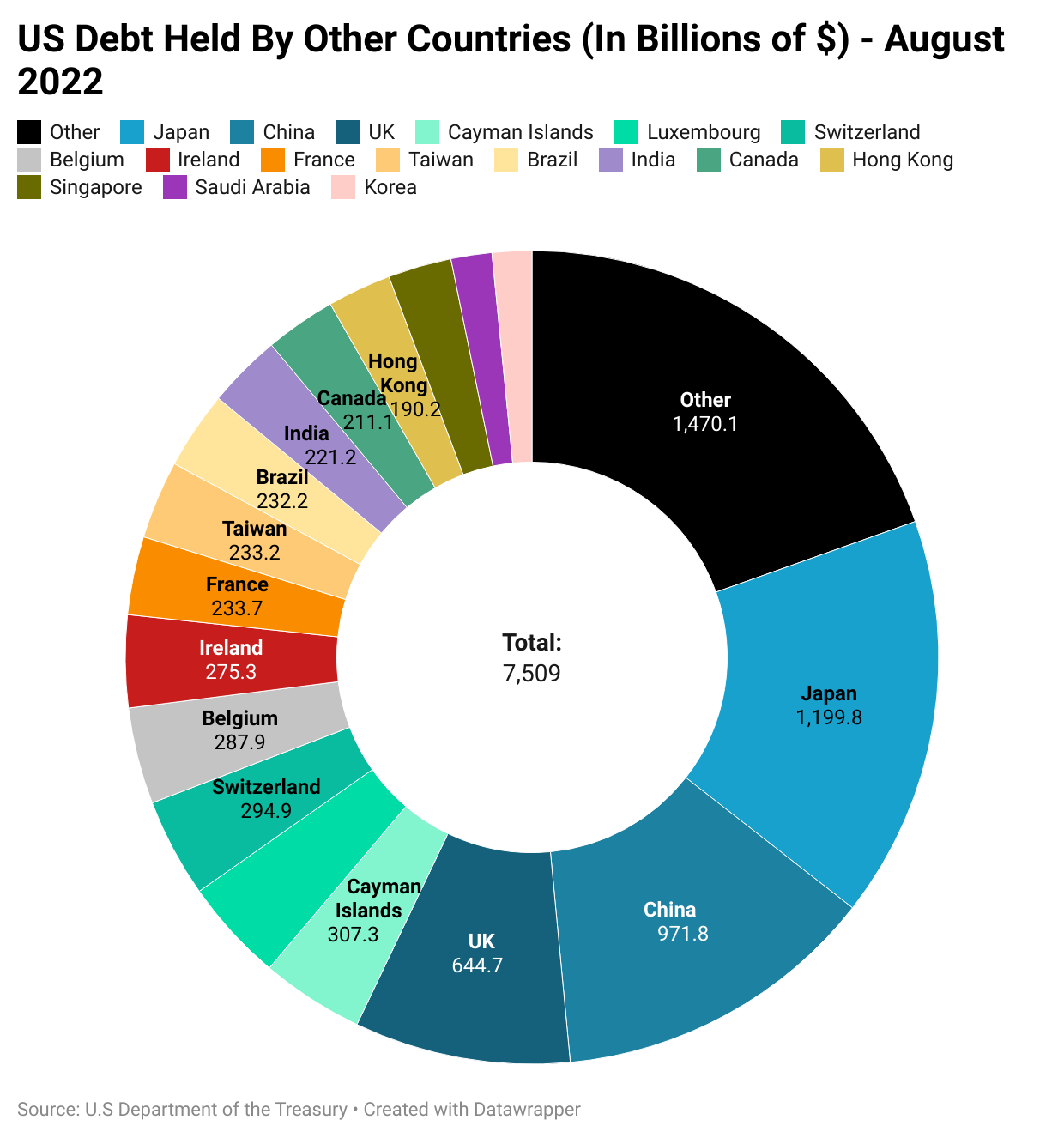

Why do no countries’ governments want to buy US debt? Well, the world’s reserve currency is the dollar. This means if countries hold debt in a different currency than their own, it is most likely in dollars because the world trades and transacts in dollars. But if you hold a lot of dollar debt, which a lot of the world does, then as US interest rates rise you are paying more interest on this debt.

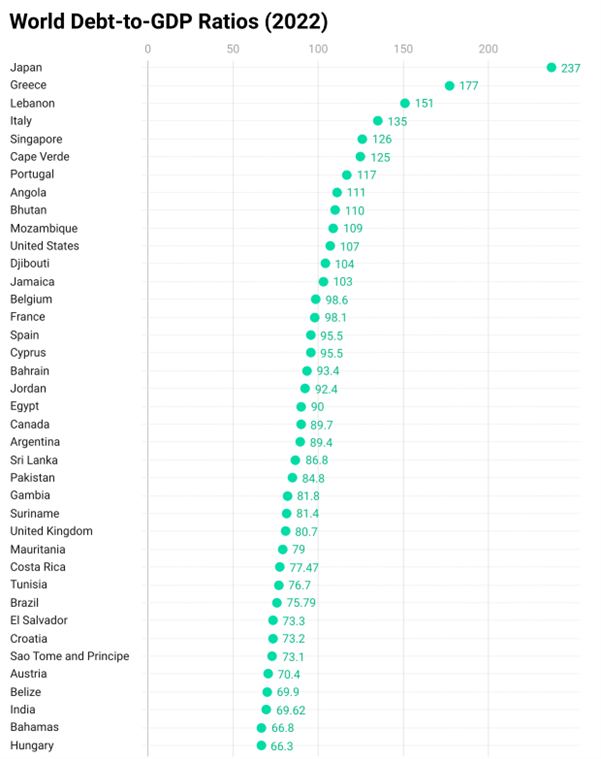

This isn’t appealing to any other country and so is leading to nobody buying more US debt, or countries even trying to sell it. Look at the Bank of Japan, their debt-to-GDP ratio is 237%. And they hold the largest dollar debt of any country in the world.

So what can countries do to incite more bond buying? In short, induce more confidence in their bond markets. This would come with getting inflation under control and lowering interest rates, before something breaks. With nobody wanting to buy US bonds, will they have to buy their own if it reaches this? This would only make inflation worse (although with 7.7% today are we beginning the way down, or just a small reprieve?).

The Bank of Japan, the Reserve Bank of Australia and the European Central Bank have installed some form of yield curve control in the past. Here is the story of the US yield curve control in the Second World War.

A Story of US Yield Curve Control (1942-1951)

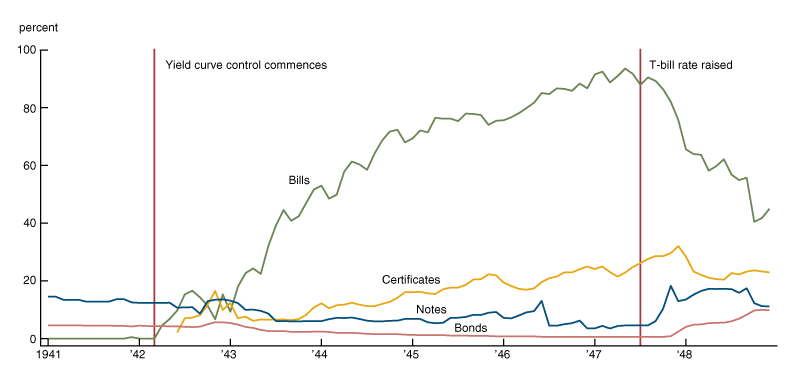

The US used yield curve control as a method to fund debt during World War Two. They pegged short-term rates and placed a cap on long-term rates. In this piece, it mentions the FOMC noted it had studied this period and the yield curve control in Japan and Australia. They said this in October 2021, so it’s already a potential tool should it be suitable.

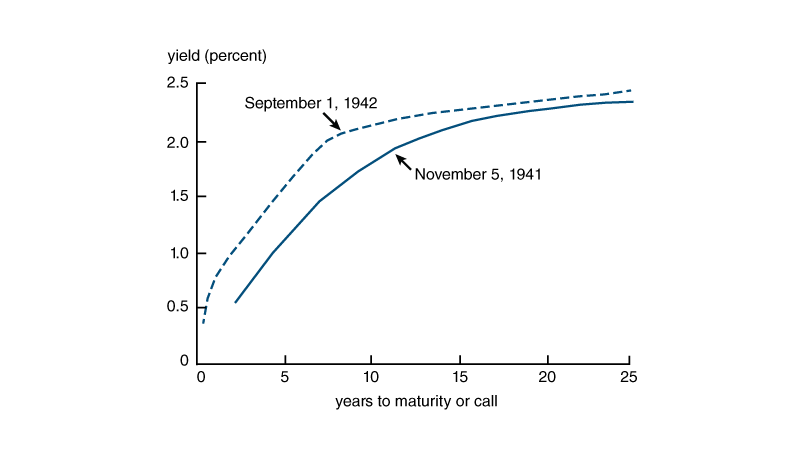

In 1942, the yield curve steepened in an upward-sloping curve due to a lack of investor demand. Another difference was in 1942 it was to fund an ongoing war effort. This time it would be people paying back stimulus checks that they received.

So who are the potential players? Well taking a look here we see a large rise in bills starting in 1943. This came as the Fed announced they would buy bills at 0.375%, but that they would also sell them to banks at this rate. This led banks to convert their excess reserves to T-bills as they had a risk-free investment of 0.375%. They could buy them and sell them back to the FED at the same rate. So it wasn’t the public after 1943 who were buying US debt. It was banks.

By the FED stating they will buy and sell treasuries at a certain yield, they are instilling confidence and incentivising banks to buy bonds.

This yield curve control was stopped in the Treasury-Federal Reserve Accord in 1951. One key lesson here was the long-term yields rose after the controls ended. Thus long-term bond prices dropped. This led to losses for investors holding them. So would yield curve control today incite more buying of shorter-term rates?

Bank Bail-Ins

If we can’t see a way out we could start from scratch with a central bank digital currency. Personal interchangeable interest rates would bring in massive income for central banks without the middleman of the banks.

In 1933, the currency used to be backed by gold. The government had spent a lot of money to try to support the economy after The Great Depression. We saw gold confiscated from people in Executive Order 6102. The government under Franklin D Roosevelt confiscated all gold and forced citizens to sell it below market price. They then set the rate of gold at $35 per troy ounce and saw the value of gold holdings skyrocket.

Today, governments are buying gold at the fastest rate in 55 years. I’m not sure what this could be leading to but it is interesting, nonetheless. Collateral or backing for a central bank digital currency? Or trying to reduce the amount of backing a rival central bank digital currency could have by buying gold? Looking to take advantage of commodity scarcity and potentially higher prices if interest rates drop, the dollar index drops and commodities rally? Who knows.

In the Great Financial Crisis in 2008, we saw a bailout in which the government used taxpayer money to support these banks. But since then we’ve seen the creation of a bank bail-in. Through a bank bail-in, detailed in the Dodd-Frank Act, depositors' and bondholders’ money is used to restructuring a bank's balance sheet to not collapse. They convert debt to equity. Small accounts will not be liable for this—only depositors who have more than $250,000. One example of a bail-in was in Cyprus in 2012-2013.

Some things in the financial system of the world are too big to fail. So it's up to ordinary people to bail them out. A bank bail-in will do this for people with big enough accounts. So how to protect yourself from this if it happened?

Spread your money and keep it below the threshold at which your capital could be used in a bail-in. Keep updated with this limit because if it changes, it would be quite a shock if a bail-in was necessary. In short, stay updated and stay vigilant about the stability of financial markets and banking.

The Story of China and US Debt

Since 2017, China has been reducing their holdings of US debt. They saw the debt of the US growing and the money printing to fund their budget deficit, and it can only lead to inflation and higher interest rates. This would impact any holder of US debt. So they decided to start to loosen their dependence on the dollar. Then when Russia invaded Ukraine, the US froze a part of Russia’s foreign exchange reserves denominated in dollars. If the US does it to Russia they will do it to any other country they deem to be a rival potential superpower. This move lost a lot of global trust in the US dollar. Even during wars, countries continue to pay their debts to each other. The financial system of debt works on trust, and the US action here will hinder Russia but led to international levels of distrust in the dollar rising.

The bond market is where the real crisis will occur. Stock market valuations are overinflated through low-interest-rate debt-funded expansion. A return to mean reversion and more sustainable valuations is due. But if there is a crisis involving the bond market, the national debt is affected, and a dollar debt domino effect would have major ramifications all over the world. This would be “something breaking” in glorious fashion.

Is a decrease in debt-to-GDP due to deflation? Not while supply shortages exist. That implies inflation not returning to the expected 2-3%. We discuss the end of globalization being upon us. And glocalization being here. Smaller supply chains. But it's a pivot of the centre of the trading world from the West to the East.

Countries that aren’t involved in China’s trading circle will have to pay higher prices as a consequence. The US is isolating itself from global trade. Will they take their closest allies from the west with them into isolation, or is it every man for himself?

This is the most unorganised writing I’ve done in a long time. And it left me with more questions than answers.

With inflation at 7.7% today YoY, are we starting to see it drop? Yields dropped rapidly so some market participants are seeing bonds as attractive. Also, this means less stress on pension funds and similar funds that hold national debt.

Will something break before inflation is fully under control (if it can ever get back to 2-3%)? If something breaks in a market outside the US, do they intervene? Is intervention even needed? If a bank fails a bail-in should solve the problem.

How quickly would the FED cut rates once it reaches this point?

If yield curve control isn’t necessary for this crisis, will it reach a point of extremes where it is? Or can the US scale back its unsustainable debt levels?

Thanks for reading! If you want more like this then follow me on Twitter or subscribe on Substack for these posts directly to your email inbox. I write and research geopolitics and financial markets to organise my own thoughts and prepare myself for anything I can control. If any of this helps you to be more prepared and ease your mind, then that’s great. If you like what you read please share it with others.