Goehring and Rozencwajg Q1 2023 Paper - Key Takeaways

Goehring and Rozencwajg Q1 2023 Paper - Key Takeaways

Link: http://gorozen.com/research/commentaries

Glossary

· b/d – Barrels per day.

· G&R - Goehring and Rozencwajg

I’m going to post this exclusively to my Substack. While I’m home for a few days, I decided to read the latest Goehring and Rozencwajg research piece and I learn better by writing down the key points. After writing down these key points, it makes sense to publish them for others to gain value from. So an extra post this week. Don’t say I never give you anything!

After breaking down the entire In Gold We Trust report, I only detail the key takeaways from the oil markets in this short piece.

1) Based on modelling, non-OPEC supply will begin to decrease by 200,000-400,000 b/d annually.

2) The global opinion was that oil demand would hit a peak in 2019 before declining. However, we have seen the opposite. Q1 2019 demand was 99m b/d. Q1 2023 demand was over 102m b/d. With seasonality and China’s reopening (if it ever has an effect, their consumer spending is looking weak), Q4 2023 demand could be over 104m b/d.

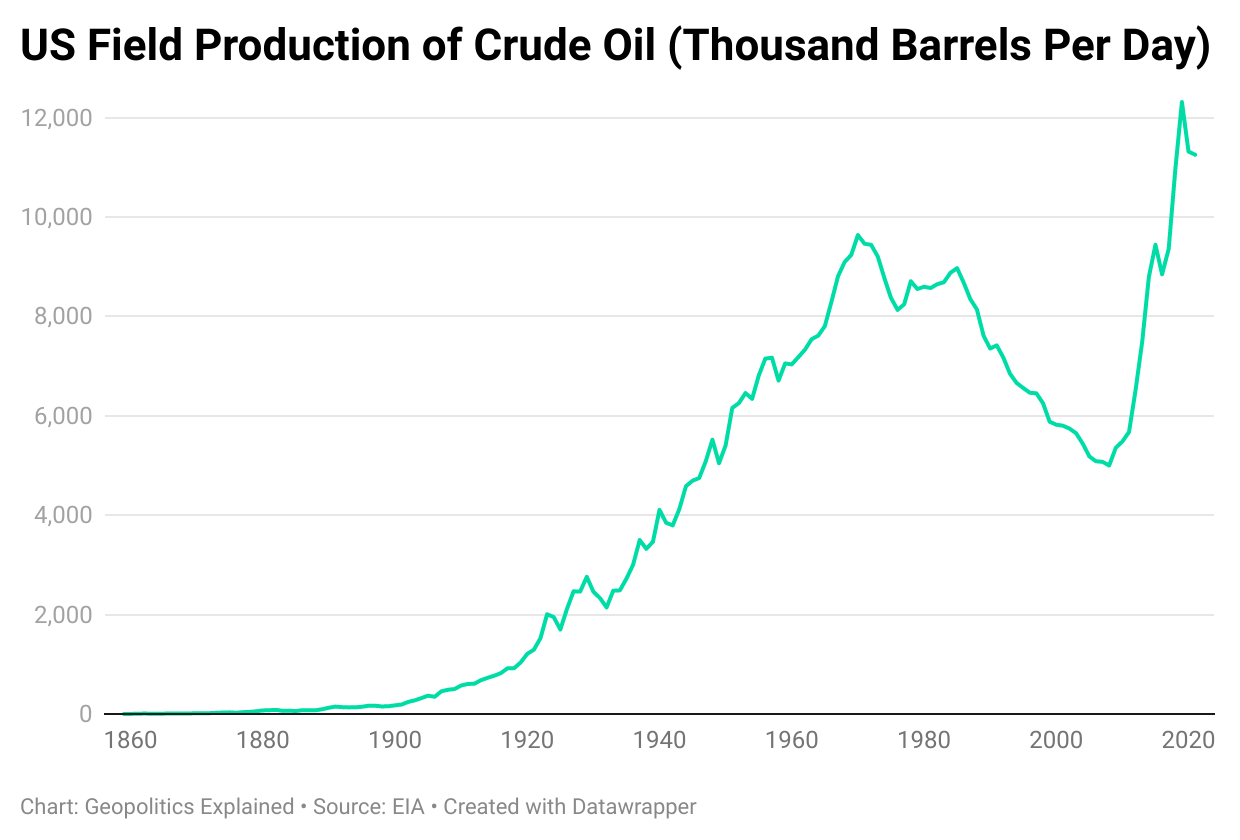

3) The only growing basin that isn’t an OPEC basin is the Permian in West Texas. The Permian is now 100% responsible for all global production growth. But not for long. Goehring and Rozencwajg originally predicted in 2018 that the Permian would peak in 2025. They now believe the Permian will hit peak production in the next 12 months.

4) Strategic reserve releases have muted prices. But OPEC production cuts are fighting the opposite side of this. Which side gives first? G&R state “the implications (of the Permian peaking) will be as profound as when United States production peaked in 1970”.

5) The shale revolution came at the perfect time. It took the US from 0 to 10m b/d of shale production, and the title of the world’s largest oil producer. China joined the World Trade Organisation in 2003 and along with it came the demand of the world’s largest consumer.

6) Shale production between 2013 and 2017, the average shale well went from 70,000 barrels of oil to 140,000 barrels over the first twelve months of activity. Technological advancement in drilling made this possible. However, this increased production depleted the best shale sources early.

7) The earliest developed basins were the Eagle Ford and Bakken. The last was the Permian. Eagle Ford and Bakken now haven’t grown in production since November 2020. G&R predict the Permian will be next and Hubbert’s Peak will reach its turning point once again.

8) Hubbert’s predicted that a basin would peak once half of the recoverable reserves had been produced. G&R count 7 billion barrels of recoverable oil in Eagle Ford and 9 billion in Bakken. These have been 65% and 55% produced respectively.

9) Commodities vs Dow Jones Industrial Average, as discussed in my breakdown of the In Gold We Trust report, shows commodities are incredibly undervalued by historical standards. The only times that were close to this level of undervalued were 1929, 1969, and 1999. After each of these periods, commodities and natural resource-related investments outperformed. Edward Chancellor’s “Capital Cycles” explains the commodity's capital cycle and the reasons for its rises and declines.

10) The conditions in place for a commodities bull market:

- Commodities have pulled back more than 70% in price since 2010.

- This commodity bear market impacted cash generation in the commodities industry.

- Companies have cut capital spending.

- Money creation reached extremes through quantitative easing.

- Easy credit has contributed to an everything bubble.

The only missing element is a shift in the global monetary system. Talks of de-dollarisation have re-emerged recently. While this will take time, countries looking to settle trade in alternative currencies is a shift in attitude towards the dollar. Countries no longer want to be victims of the weaponization of the dollar.

11) If China seeks to displace the USD, gold convertibility via the Shanghai gold exchange will be vital. China’s rapid accumulation of gold in recent quarters makes this more plausible. Commodity bear markets in the past have ended with a shift in the global monetary system and a dollar devaluation.

12) For a review of Q1 2023 in terms of commodity performance, this is included in G&R’s Q1 2023 Market Commentary section. I won’t cover this here.

13) In the past, Saudi Arabia was cautious about production cuts reducing their market share. They no longer view the shales as having significant potential to impede their market share.

Leigh Goehring was recently a guest on Macro Voices, where they discussed an impending food crisis occurring over the next decade in agriculture. They also discuss Gleissberg Cycles and sun spots, as I discuss here in my post about the present-day scene of the energy industry.

Thanks for reading! If you want more like this then follow me on Twitter or Medium or subscribe on Substack for these posts directly to your email inbox. I write and research geopolitics and financial markets to organise my own thoughts and prepare myself for anything I can control. If any of this helps you to be more prepared and ease your mind, then that’s great. If you like what you read please share it with others.

Geopolitics Database: https://www.geopoliticsexplained.co.uk/geopoliticsdatabase-access

Geopolitics Explained Podcast:

https://www.geopoliticsexplained.co.uk/geopol-podcast

or listen here:

If you enjoy the books I breakdown, you can purchase them here, along with affiliate links to the books and a 30-day free trial of Audible:

www.geopoliticsexplained.co.uk/book-takeaways

If you like what I do here, please like or share this post. You can also buy me a coffee or the next book I can discuss in the current reading section: https://www.buymeacoffee.com/geopoliticsexp