The Future of Cryptocurrency – Recent Events Have Caused Damage, Can We Regain Trust?

The Future of Cryptocurrency – Recent Events Have Caused Damage, Can We Regain Trust?

Contents

1. Introduction

2. Crypto Part 1: How Centralised We Really Are

2.1. DeFi vs CeFi vs TradFi

2.2. The Blockchain

2.3. The Aims of Crypto

3. Crypto Part 2: Regulation

3.1. A Free and Permissionless Internet – Should Crypto Be Too?

3.2. Central Bank Digital Currencies and Stablecoins

3.3. Countries’ Crackdowns on Crypto

4. Crypto Part 3 – FTX

4.1. The Collapse of Firms That Led Us to FTX Collapse

4.2. FTX and Alameda – A Relationship Within A Relationship

4.3. SBF and Government

4.4. A Run: Traditional Banking vs Cryptocurrency Exchanges

4.5. ICOs and How To Regulate Them

4.6. Who is At Risk Now

5. Concluding Remarks

References

1) Introduction

I’ve been wanting to write a longer form, paper-style document for a while. The implosion of FTX in the cryptocurrency industry made for a brilliant opportunity to do so. There is so much to talk about. How the FTX collapse has brought to light decentralised finance, centralised finance, and traditional finance. Regulation. Central Bank Digital Currencies. And all this is before unpacking the FTX situation.

I wrote these sections at different times as individual pieces, so I’d recommend you read them in such a way. I could repeat myself and it will sometimes be disjointed. But I want to get this out before things change even more!

Note, some sections are opinions and me teaching myself about these recent events. If there are any mistakes, or new truths are revealed that leave some of what I’ve written incorrect, please let me know and I will provide updates to this piece. I’d love anybody’s ideas on the things I discuss. I know technical details about the entire crypto industry at an average level. Much of the things I discuss are through research for this piece. I hope you learn something from my research. I know I did, and I have a much clearer view of the cryptocurrency field now and where the future might take us.

2) Crypto Part 1: How Centralised We Really Are

Sam Bankman-Fried (SBF) is the biggest name in the world of crypto. His crypto exchange FTX, where you could buy cryptocurrencies was one of the most popular. “Was” is the important word. Last week FTX filed for bankruptcy. I’m going to tell the story in detail, which actually started a month ago. I’ll discuss its impact, and where we’re heading.

First I’ll explain some terms involved in the crypto market because my Mum reads my posts and I need the free likes she gives me.

2.1) DeFi vs CeFi vs TradFi

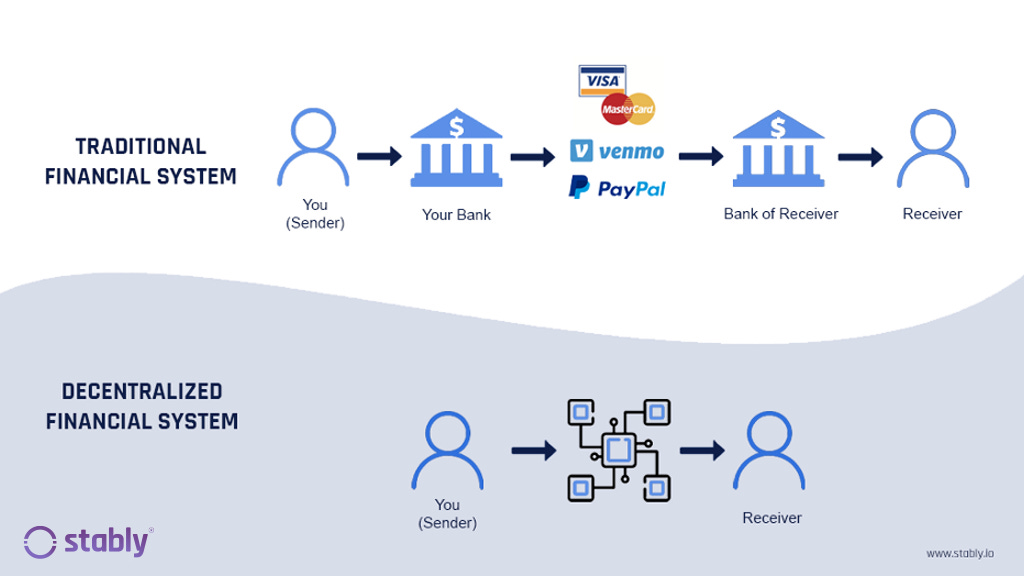

Decentralised finance is finance without the middleman. In the current traditional finance system, if Dave wants to send money to Jim, he does so through a bank who can see a lot of information about this transaction. In decentralised finance, Dave will send the funds directly to Jim using a wallet code. Each wallet refers to a singular cryptocurrency coin. So, Dave could send bitcoin from his bitcoin-specific wallet to Jim’s bitcoin-specific wallet.

CeFi exchanges offer cryptocurrencies, but you often have to verify your identity through know-your-customer (KYC) checks. Examples of these are the most well-known exchanges such as Binance and Coinbase.

There are different types of wallets. A soft wallet is a digital wallet that can be accessed with a number of words to secure it. You can access a wallet through the computer, often as google extensions, or through apps on a phone. A hard wallet is a physical wallet. A soft wallet is susceptible to hacks so choosing a popular, secure one is particularly important. A hard wallet will need physical protection and storage. If you lose it, you lose your funds. You can access a hard wallet via a private key once the device is connected to a computer.

If you hear the terms hot wallet, it refers to one connected or hosted on the internet. If you hear cold wallet, it is one where assets are stored offline.

Wallets are free to download and don’t charge for storing your assets. They make money by charging a small fee for transactions or staking to earn more on your cryptocurrencies at a certain percentage by locking them away, for a specific period of time.

2.2) The Blockchain

The blockchain is what stores the cryptocurrency sector. It is a ledger, or database, which records all transactions and tracks assets. It is shared on a network and stores the information electronically. The transactions are secure and decentralised. This is what generates trust in crypto transactions without the need for a middle party such as a bank.

The blockchain data is organised into blocks, that like any digital storage system, have storage limits. Once these are filled, the block is closed, and a new block is established. This new block is linked to the old block, in a blockchain. Clever name, right?

Crypto stored in an exchange is crypto that isn’t on the blockchain. The blockchain is the most secure place for personal crypto funds. Get them in a wallet that is on the blockchain.

The blockchain stores many aspects of the cryptocurrency sphere, such as different cryptocurrencies, decentralised finance (DeFi) applications, non-fungible tokens (NFTs), and smart contracts.

Note, even though they are called cryptocurrencies, not all of them act like currencies. The largest by market cap that act like currencies are Bitcoin (BTC) and Litecoin (LTC). Some cryptocurrencies track a specific blockchain and represent that blockchain, powered through an asset, such as Ethereum (ETH), Cardano (ADA), and Solana (SOL). Some cryptocurrencies allow for communication between these blockchains such as Chainlink (LINK) and some are decentralised cryptocurrency exchanges where you can buy all these assets, such as Uniswap (UNI). There are many other uses for other cryptocurrencies.

2.3) The Aims of Crypto

The cryptocurrency industry wants to change the financial system to add privacy and remove control. In the traditional financial system, there is control given to the banks and governments, a lack of privacy and inflation. Crypto offers the exact opposite of this. Control returns to the people, with privacy but the ledger of transactions is still open source, so all transactions are public but unable to be tied to a specific person publicly. Finally, some cryptocurrencies have a fixed total supply. This fixed supply is first accessed by crypto mining.

Crypto mining is the process through which new cryptocurrency is created and enters circulation. This is done by solving mathematical problems and validating transactions, as an auditor. This stops copies of digital currencies from being made. The first computer to complete the problem receives the block of bitcoins. Mining is known for being very energy extensive through the large amounts of electricity used. This is because if you want your computer to complete the problem the quickest, you need a powerful computer to do this, which in turn uses a lot of energy.

The supply that is mined is released over time, but less and less supply is released over time. This means the same number of people will be trying to mine a smaller amount of cryptocurrency over time. This should drive up the price of cryptocurrencies over time.

But because the total supply is fixed, this leads to no inflation in these coins. Hence these cryptocurrencies don’t experience devaluations and don’t lose value over time through inflationary pressures.

This is why cryptocurrencies can be seen as a hedge to counter traditional fiat currency. As central banks print money, a fiat currency loses value because there is a greater supply. This is one advantage of crypto that doesn’t lose value through supply increases and inflation.

3) Crypto Part 2: Regulation

SBF published a post to Twitter and the FTX US website titled “Possible Digital Asset Industry Standards.” In short, it detailed a midway stop on the path towards regulation in the cryptocurrency market.

His post openly welcomed feedback from the crypto community. And he received quite a lot of feedback, most notably from Erik Voorhees.

SBF was a guest on the Bankless podcast on October 29th where he and Voorhees debated the contents of his draft for crypto regulation. The key points I gauged from that interview:

· Under the SBF draft, decentralised finance would die.

· The DCCPA

· OFAC vs NOFAC

· The Bank Secrecy Act

In the debate, Voorhees destroyed SBF’s draft in a calm and thoughtful approach, bringing up many counterarguments for why the draft would surrender control of decentralised finance to governments and breaking the critical principle of cryptocurrencies that they are permissionless and free from control.

The DCCPA is a leaked bill that details cryptocurrency regulation. It stands for the Digital Commodities Consumer Protection Act. The act will kill DeFi. The term “digital commodity trading facility” is included in the DCCPA and would exclude parties who develop or publish software.

CeFi exchange Coinbase’s CEO, and SBF were openly in the agreement with the bill. Of course, the two are in direct competition for cryptocurrency market engagement with decentralised exchanges. DeFi is seen as riskier due to the lack of a company backing it that could interfere if things went wrong. But this argument is also used that CeFi companies can exert too much control and use this to their advantage.

SBF in the debate interview on Bankless discussed trade-offs and how to stop cryptocurrencies from being regulated into early, permanent retirement, we might have to make some. The chances are any trade-offs in government regulation won’t benefit the crypto space’s biggest advocates due to its ideology of privacy and individual control. This could be especially true now governments could use the bankruptcy of FTX, one of the biggest CeFi, to rush through regulation, citing that its necessary for the protection of investors.

One key point that SBF made that I do agree with is that DeFi is difficult to regulate. For everyone to be happy, decentralised finance would have to remain decentralised. There could be no government organisation that inserts itself in the middle because that would no longer be decentralised. Could a newly created independent organisation that monitors fraud and frauds in the DeFi space work, without being able to influence, only monitor? As the blockchain is a public ledger, they could monitor and use tools to track down parties who use the cryptocurrency markets to commit crimes. Voorhees argues as theft, fraud, and frauds are illegal in traditional finance, they are also illegal in decentralised finance and crypto, and hence should just be punished the same. But an independent organisation could help in dealing with and combating these issues quicker.

Another issue, in the face of crimes committed by these decentralised finance projects, who would be punished? Do they have an owner? Decentralised apps are just code on a public blockchain. Smart contracts power decentralised apps and are contracts that are executed once specific criteria are met. So smart contracts play the role of middleman that exists in centralised finance.

If an attack is made on a blockchain, the attacker should be punished. If a decentralised application suffers a rug-pull where all funds are pulled out through a backdoor, then the creator of the code should be punished for coding this back door in the first place.

This leads to the Financial Action Task Force. The group set rules that define who is responsible for DeFi projects. It discusses if DeFi creators should be subject to the Virtual Asset Service Provider (VASP) regime. This leads to Anti-Money Laundering (AML) and Counter-Terrorist Financing (CFT) rules having to be followed.

The questions asked under the test are as follows:

· “Does a person or entity have control over the assets or the protocol itself”?

· “Does a person or entity have "a commercial relationship between it and customers, even if exercised through a smart contract”?

· “Does a person or entity profit from the service provided to customers”?

· “Are there other indications of an owner/operator”?

If there is no owner and a project was completely decentralised, then a VASP could need to be involved if it were regulated in this way. This could lead to decentralised apps having to contain know-your-customer (KYC) checks, which removes the anonymity of decentralised finance. This is because DeFi developers can’t perform checks that the AML and CFT impose.

My final point on DeFi regulation, is a token such as UNI for Uniswap, treated as a digital asset or a security? This varies for countries and regions. The SEC, under the “Howey Test” state that tokens are securities whereas the EU classes them as digital assets.

The Howey Test states, “an investment contract exists if there is an investment of money in a common enterprise with a reasonable expectation of profits to be derived from the efforts of others.”

One example where this causes trouble is liquidity pools. A liquidity pool works to keep liquidity in a network by rewarding participants who place assets in the pool. Trades occur within the pool and participants receive tokens as a reward. It’s a group of users who provide liquidity to a smart contract that is published through code, so is there an owner?

One similar creation to this was the internet.

3.1) A Free and Permissionless Internet – Should Crypto Be Too?

The internet is a neutral place. Network neutrality is a critical principle on the internet that details those who provide internet services (ISPs) have to treat every user equally regarding charging consistent rates for commerce.

Types of Regulation for the Internet:

· Things we say on the internet.

· Data produced and posted on the internet.

· Things we see on the internet.

· Cyber laws such as website creation, domain names, and trademarks.

· Copyright and intellectual property laws.

· Privacy laws.

· Harassment laws.

· Cybercrime laws.

· Data protection laws.

· Cybersecurity laws.

The internet is a global-spanning entity. So the regulation introduced has to be equally as deep. This is similar to cryptocurrency. A challenge to the current global financial system. So any regulation needs to be deep, and well-constructed. So what are the differences between regulating the internet and regulating cryptocurrencies?

Through internet regulation, governments had more control. Control over what people see. Control over what people are up to. As we all know, the internet can be a wonderful place, but also a terrifying place. Cryptocurrencies and DeFi would not bring government control. CeFi would, just like TradFi does. SBF was heavily involved in the DCCPA opinions, and it would have benefitted him and other CeFi companies by wiping out DeFi protocols. I can’t see how DeFi can exist with complete free reign because of the lack of influence outside parties, including governments can have on it. DeFi would also completely remove the need for banks, but without the backing and control, banks have in liquidity crises. They can be presented as dangerous and anarchic. CeFi is the answer to this danger and anarchy in the eyes of governments. Will the people think the same? Unlikely.

Even if DeFi was made illegal. Would it stop? It's open-source code on a public ledger. Wouldn’t that be an attack on free speech? Not that this is a problem nowadays with governments limiting what people say on social media if it doesn’t suit their narrative.

The regulation comes down to the government of each country which will have different laws for the citizens of its country. It is looking like cryptocurrencies will be regulated the same way. If some countries got the internet regulation right, it would be great if they could get cryptocurrency regulation correct too.

Some of the clearest approaches to crypto regulation I can find have been posted by the Bank of England.

3.2) Central Bank Digital Currencies and Stablecoins

Andrew Bailey has stated that cryptocurrencies can threaten the world’s current financial system. And their volatility can lead to rapid shifts in purchasing power.

A stablecoin is a business’s version of an asset that often provides reserves for its company. For example, Binance has BUSD. BUSD is pegged to the price of $1. As we have seen recently, sometimes pegs break. In crypto, a peg breaks due to liquidity problems. This brings the clear necessity of proof of reserves for these companies. Because currently, they are incredibly unsafe. They are meant to be a store of value, but often the collateral backing these assets is not structured in a way that promotes safety.

With FTX, we saw that most of their collateral was in their own token, FTT. This means that when they experienced liquidity problems, customers rushed to withdraw their holdings. As a large section of their reserves was held in FTT, it led to a vicious circle of prices getting lower and lower.

This is what happened with CZ, the Binance CEO. He announced he was selling his FTT holdings, and the price dropped rapidly. Alameda offered to buy the tokens that CZ dumped at $22. This was around what the price was at, so Binance would have had nothing to lose. Of course, at the time it wasn’t clear how integrated FTX, and Alameda were. So why didn’t CZ take the deal? Did he know more about FTX and their horrific financial situation than he let on? After the collapses we’ve seen this year, it’s been brought to the forefront that many crypto firms don’t have the structure of reserves and collateral needed to support a run-style event. CZ could have just foreseen this exact crisis occurring before it did.

He told his employees to not buy or sell FTT. It was rumoured that he was trying to ruin one of his closest competitors. Even if he was, it has brought to light how poorly run FTX was, and how they were exploiting believers in the crypto ideology by orchestrating a bubble environment with its own exchange and token.

We have even seen currency pegs break in fiat currencies in the past. Black Wednesday in Britain in 1992 saw the day that speculation led to the British exit from the European Exchange Rate Mechanism (ERM). The ERM managed currency exchange rates relative to other currencies. This is referred to as a fixed exchange rate. We now live in a floating exchange rate system, set by supply and demand and monetary policy is a lot more important.

Black Wednesday saw George Soros hold a massive, short position in the pound. He made this trade because he saw the rate at which the pound was pegged was too high, among other criteria. The key peg was the 1 GBP equal to 2.7 Deutschmarks (DEM). The UK upped interest rates to try to bring more people into the pound and artificially maintain prices. We’ve seen how artificially trying to maintain prices goes. So the British gave in and withdrew from the ERM.

The difference between central banks backing a fiat currency and businesses backing a stablecoin comes down to debt markets. Countries raise money through their bond markets. A purchaser of a bond trusts that they will get their money back at the bond’s maturity. This debt can be used to support an economy. In crypto, these businesses should make money from fees when people buy or sell. The recent collapses of many crypto companies make it clear that some used customer deposits to try to grow their own profits or back their own business with collateral in a token of their own creation.

In short, they got greedy. And customers are the ones who suffer from the irresponsible financial approach of these management teams.

Proof of reserves is necessary. Regulation is needed here regarding CeFi company financial accounts, reserves, liquidity of assets, and uses of customer deposits. Incredibly high yields in yield farming are unsustainable and set stupidly high targets that companies have to increase income by to support. Crypto has been about bigger and better for years. It needs to get smaller, and back to basics. Trust the ideology and technology behind it. And keep a keen eye out for those taking advantage and trying to fill their own pockets. This could be a deep routed problem in CeFi, and an argument for the absolute necessity of DeFi.

Cryptocurrencies aren’t productive and have no value. A lot of them perform a function, but unless they can be used in everyday purchasing, they are just financial assets and a hedge against other asset movements such as fiat currencies and gold. Bailey states “they have extrinsic value as people value things for personal reasons. But they don’t have intrinsic value.”

One digital asset that would have intrinsic value according to central banks is a central bank digital currency. But it is just like CeFi and TradFi. Control isn’t with the depositor. In fact, control for the depositor is even smaller because everything is digital. Cash would be experiencing a dramatic death. COVID accelerated this drastically as everyone turned to online commerce and as little contact with others as possible. Cash withdrawals were 60% lower in April 2020 vs April 2019.

So, will CBDCs and stablecoins exist together, harmoniously?

The answer is most probably, yes. Stablecoins are supposed to be backed by large amounts of reserves, in a variety of different assets. This could be cryptocurrencies or even fiat backing. Stablecoins are pegged to remain at a specific value. Many stablecoins track the value of one US dollar.

Most crypto assets are volatile, making them unsuitable as a store of value. But stablecoins solve this issue.

However, the key point is this:

“If stablecoins are to be widely used as a means of payment, they must have equivalent standards to those that are in place today for other forms of payment types and the forms of money transferred through them.“

So they have to be centralised. That makes them no better than CBDCs. If anything, it actually makes them worse because the lack of transparency and regulation leads to issues. The stablecoin asset class is arguably where this distrust in the crypto space started. Specifically with Luna and Terra.

But, just like most crypto, stablecoins won’t be accepted as legal tender. Stablecoins can be pegged to a dollar, or digital dollar and be used as currency in a crypto ecosystem. And every country will be different. Just like El Salvador accept BTC as legal tender, some countries could accept a stablecoin pegged to the dollar as legal tender. The dollar is the global reserve currency and is currently the least dirty shirt in the pile when it comes to global currencies in a rising interest rate economic environment. But these countries are often ones with poor economic conditions such as hyperinflation, massive budget deficits, or high levels of debt they can’t afford to pay as they produce little.

A promising point of the Andrew Bailey BoE papers is he states innovation is a good thing and it is not in authorities' and regulators' interest to stop innovation. If some crypto innovation will make the financial system a better place, it will be heavily considered. They are also aware of the privacy issues that spenders of a digital currency would have to suffer from.

“The data generated could have huge opportunities for the detection and prevention of financial crime, but this must be balanced with the risk of surveillance into private financial matters.”

This openness to innovation in the UK is better than in countries where it is banned completely.

3.3) Countries’ Crackdowns on Crypto

Nine countries have banned cryptocurrency completely. It is illegal in these countries:

· Algeria

· Bangladesh

· China

· Egypt

· Iraq

· Morocco

· Nepal

· Qatar

· Tunisia

Another forty-two countries have implicit bans so financial institutions in the country can’t adopt cryptocurrency companies as clients. The countries are as follows:

· Bolivia

· Ecuador

· Guyana

· Bahrain

· Georgia

· Indonesia

· Jordan

· Kazakhstan

· Kuwait

· Lebanon

· Macao

· Maldives

· Moldova

· Oman

· Pakistan

· Palau

· Saudi Arabia

· Tajikistan

· Turkey

· Turkmenistan

· UAE

· Vietnam

· Benin

· Burkina Faso

· Burundi

· Cameroon

· Central African Republic

· Chad

· Côte d’Ivoire

· DRC

· Gabon

· Lesotho

· Libya

· Mali

· Namibia

· Niger

· Nigeria

· Republic of the Congo

· Senegal

· Tanzania

· Togo

· Zimbabwe

This accounts for over a quarter of all countries in the world (195 total). One key aspect of these bans I can think of is the idea of keeping money within a country. Crypto enables the cross-border sending of funds. If these countries aren’t very productive countries and aren’t involved in global trade on a large scale, they will want to hold as much capital within the country as possible.

Although these countries ban crypto, that doesn’t stop them from assessing and considering the underlying technology that cryptocurrencies are built on such as the blockchain.

I, for one, am excited about how future tech could be implemented into the world. Artificial intelligence. Specifically machine learning algorithms such as neural networks. Also, quantum computing excites me. This technology could monitor the crypto market for sentiment, liquidity, and volatility by learning from previous patterns and data. Being able to locate problems quicker, especially with liquidity could be aided through the use of AI. It would bring greater transparency.

The new technology could drastically shift and aid the cryptocurrency industry. Whether that is in centralised or decentralised systems, innovation is key to our development as a people. Technology that can be accessed anywhere on the globe, in an unlimited, permissionless way will raise the entirety of humanity. It could take a long time; I have no guess on any sort of timeline. But the goal of us all should be to raise all of humanity up to achieve things we never thought possible.

4) Crypto Part 3 – FTX

4.1) The Collapse of Firms That Led Us to FTX Collapse

Firms We Have Seen Collapse or Have Liquidity Troubles:

· 3AC

· Luna

· Voyager

· Celsius - FTX sent Celsius USDC to support their exchange.

· Gemini

· BlockFi

· Nexo

The collapse of many of these firms led to FTX bailouts to keep them afloat and increase liquidity. Why would they do that? To cover up their debt exposure to these firms collapsing? These were illiquid platforms and liquidity is the key driver of crypto markets and maintaining stability in the markets. All these firms are interconnected, and FTX made that even more of a problem with these bailouts. Due to the lack of regulation with crypto financial accounts, bad decisions can be hidden well. They were especially hidden well when the debt was cheap. Now that the macro environment has shifted to risk-off, debt is more costly and the stupid financial decisions to appear stronger as a business are exposed. When they're all interconnected, one collapse leads to further potential collapse.

Sidenote: I lost $5 of bitcoin in BlockFi, and this loss is going to financially ruin my family. In all seriousness, this is a lesson to move money off crypto exchanges into a wallet where it’s under the control of the purchaser, not the platform from which it was purchased upon.

4.2) FTX and Alameda – A Relationship Within A Relationship

The fact that FTX and Alameda filed for chapter 11 bankruptcy at the same time is telling of the clear links between the two. They were completely integrated with each other, under one system. FTX for bringing in customer capital. Alameda for using that customer capital for their own gains.

FTX is a centralised cryptocurrency exchange where crypto can be bought by market participants. Alameda is a trading firm, also founded by Sam Bankman-Fried. The story writes itself. So much so that Amazon has signed a deal for an 8-part series, directed by the Russo Brothers. I can't wait to see what other details come out of this.

Alameda was actually the company set up first by SBF in 2017. He set up FTX in 2019, most probably after realising how easy it is to get away with things in the cryptocurrency sector. It has only been realised due to the macro environment we find ourselves in. In the long run, they do not get away with this. We have seen Elizabeth Holmes, founder of Theranos, jailed for 11 years. Fraud is not taken lightly. Time is taken to collect all the facts and as SBF currently roams freely around the Bahamas, the Elizabeth Holmes trial is the most recent reminder of how fraud cases do reach a conclusion with time. This is a clear failure of CeFi and reinforces the point of owning your own crypto in a wallet.

4.3) SBF and Government

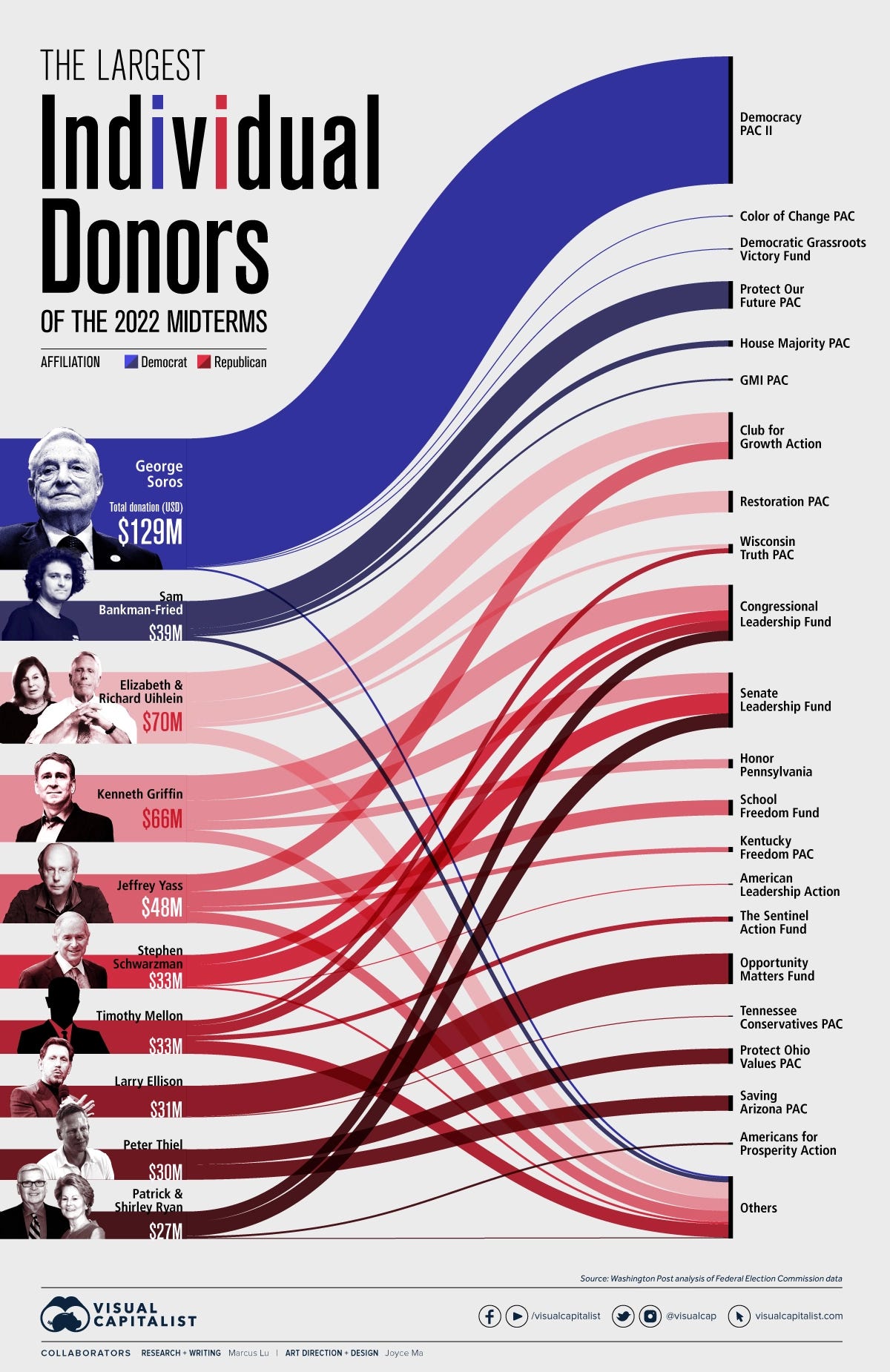

A key aspect I haven't mentioned is how tied into the government SBF was. One of Erik Voorhees' main points was because SBF was so heavily involved in the regulation through DCCPA, he had the sway and influence to impact its details. But as CEO of a centralised finance exchange, he would have benefitted from the regulation of DeFi, so he wasn't going to agree with Voorhees there. Also, SBF was the second biggest donator to the democrats for the midterm elections at $39 million. Only George Soros was a bigger donator

.

However, SBF also sent money to the republicans and people close to him did too. SBF was covering all the bases depending on which party was in power.

Another interesting development was SBF's relationship with Gary Gensler and Glenn Ellison.

So, SBF dated Caroline Ellison, who is the CEO of Alameda. Glenn Ellison is Caroline Ellison's father and is the former boss of Gary Gensler who is the current head of the SEC. This originated when they were both professors at M.I.T. Who else went to M.I.T? SBF. The ties to the government are clear. SBF had a massive influence when it comes to crypto regulation. Could he still have influence and the bankruptcy of FTX be used to regulate crypto, specifically DeFi, under harsh terms that kill the permissionless environment?

The FTX black hole was around $8bn. Where did this customer's money go? Well, it went to Alameda. Over at Alameda, they were trading customer funds in an attempt to increase their capital. This was demonstrated through yield farming. Yield farming is where you deposit your cryptocurrency and you earn a yield on it, similar to depositing money at the bank and earning interest. But these yields in some cases were incredibly high. This number would excite most people by examining the future trend and extrapolating what their account balance would look like. I can see it now. Cartoon characters with dollar bills in their eyes. But, if your bank suddenly started offering you 50% interest on your money held there tomorrow, you would question it. Or those of us who consider underlying risk definitely would.

Crypto stereotypically attracts participants who are less interested in the ideology behind cryptocurrencies, that they are permissionless and out of the influence of the government, central banks, and actual banks. So they care little about the risk. They just want to make massive returns that aren’t offered anywhere else in the financial markets. Massive yields can only highlight the massive risk being taken with customer capital. I don’t understand how crypto participants don’t understand their capital is at incredible risk under these systems.

This isn’t just an FTX strategy. Many CeFi and DeFi crypto firms offer yield farming. The yields offered on CeFi exchanges are a lot more sustainable than DeFi yields stereotypically which can be in the thousands.

It is a constant squeeze on liquidity until too much capital is locked away in illiquid assets to try to maintain these yields. When a large rush of customers wants to get their money off an exchange, and the exchange experiences a run, they don’t have enough liquid assets to cover all the customer withdrawals. Hence bankruptcy.

It is called fractional banking and on paper, sounds incredibly similar to how regular banks operate. They only require a small fraction of bank deposits to be backed by actual money that is available for withdrawal. So what are the differences between when banks do this and when crypto firms do this?

4.4) A Run: Traditional Banking vs Cryptocurrency Exchanges

As mentioned, when a run occurs on a traditional bank, other banks offer short-term loans to each other in order to maintain order in the global financial system. It is more effort to have a bank default, so they all lend to each other to maintain liquidity for those banks who need it.

This post here breaks down bank runs fantastically and much better than I could, so for more information refer to this.

A run on a cryptocurrency exchange is a completely different beast. As we saw in the FTX story, at one point, Binance was going to bail out FTX by purchasing its FTT token. But, CZ, the Binance CEO, ultimately decided against it. Will CZ come to regret this due to how integrated FTX was in the cryptocurrency sector? Many cryptocurrency businesses have investments and assets in other businesses.

If Binance emerges from this cryptocurrency potential liquidity crisis with its exchange still intact, it will be the largest cryptocurrency exchange by quite some distance. The failure of FTX is a clear win for Binance from this perspective.

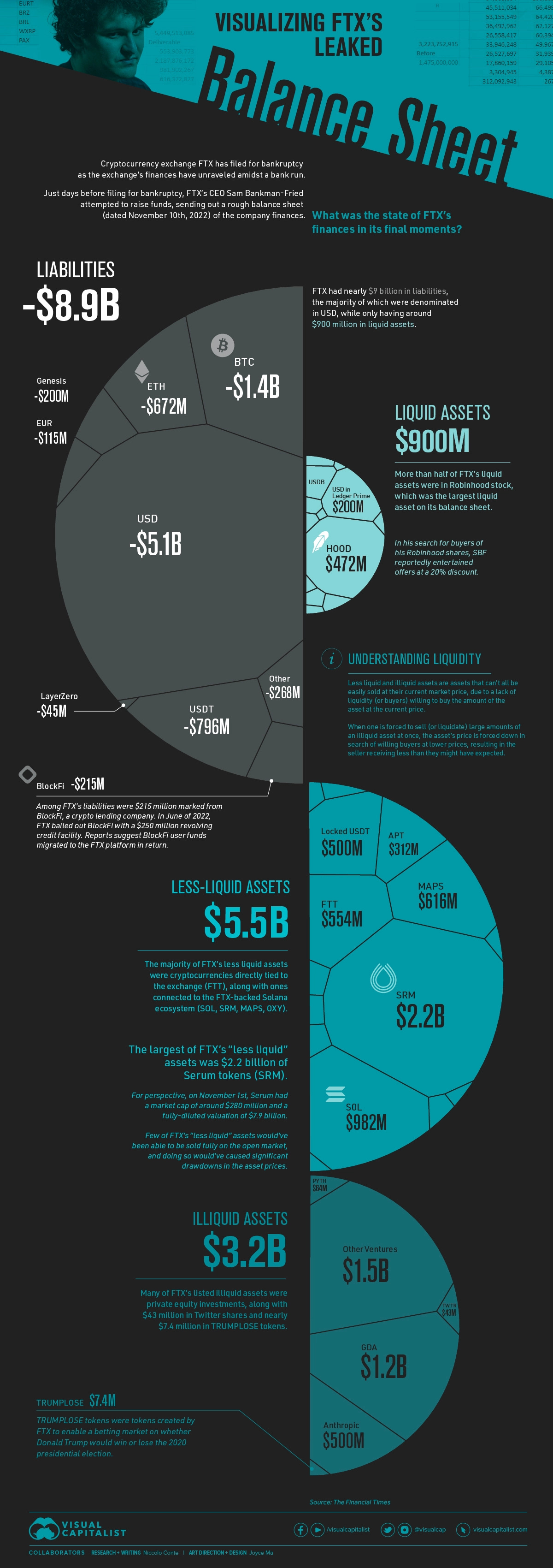

An alternative reason for pulling out of the deal could have been regarding the state of FTX’s financials. It states how poorly run FTX was when they had $900m liquid assets against $8.9bn liabilities. In a rising interest rate environment where debt interest payments are costing even more, this was a reckless disregard for the security of customer funds. No company would want to take on this debt in a rising interest rate environment. It’s not worth the risk. It is especially not worth the risk for Binance, which is a clear industry leader as a CeFi exchange, should they battle through the crypto winter.

So, this exact scenario demonstrates the support for cryptocurrency exchanges in a run scenario. It doesn’t matter if they’re CeFi or DeFi. FTX didn’t have enough liquid assets when customers were rushing to get their money out. They couldn’t access liquid assets quickly enough without taking on even more debt if they even got approved. And no other cryptocurrency exchanges would bail them out by offering capital to support them, because all these exchanges are in direct competition for crypto market share.

Banks support each other in liquidity crises because it appeals to them to lend to each other at the federal funds rate and receive interest payments back. This also helps banks meet their daily reserve requirements. Everyone benefits.

In crypto, just like geopolitics, it is much more about self-interest. Of course, I’m sure the banks are too but we see strategic partnerships where it's mutually beneficial for both parties. In crypto, it is not mutually beneficial. And so we see collapses due to reckless financial structures of these companies trying to capitalize on low-interest rate growth that has suddenly ended and left them overexposed to debt, with too few liquid assets to cover.

The competition led to wacky offers in yields, as customers sought returns on their cryptocurrency as it sat there being unproductive. More pressure on these exchanges to try increasingly reckless strategies to make more money to beat their competition. One exchange raises the stakes another makes. This could mean the cryptocurrency house of cards has even further to fall with more runs and bankruptcies in the space.

One small positive is that the firms who emerge from this will have learnt a valuable lesson. There will be a lot more thought put into how customer funds are stored, backed, and used to increase capital. The crypto space already has a reputation for being an incredibly bubbly sector. This causes insane volatility as customers rush for high returns. It’s like everything is going at 1000mph. It needs to slow down. Exchanges need to be backed securely and only offer sustainable yields on holdings. Productivity needs to increase in regard to the facilities and uses cryptocurrencies offer. And a less chaotic environment leading to less volatility.

Free markets allow anybody to enter any market they want. Capital is allocated through the price mechanism, competition, supply, and demand. Competition between cryptocurrencies doesn’t drive the price much, because if the entire cryptocurrency market goes up, they all go up. Its demand, for unsustainable returns, brings liquidity and volatility to cryptocurrency markets. Then it dries up after the bubble bursts.

In economics, boom and bust cycles naturally occur in our capitalist system. And the percentage that BTC rises in each boom cycle from trough to peak is reducing. Over time, could we see a crypto market that naturally becomes more stable? It would lead to more sustainable trading and investing strategies that’s for sure.

One way that new projects are launched is through initial coin offerings. This method is the cryptocurrency version of an initial public offering for a business outside the crypto space. This is one of the key places I would want to see regulation. As Erik Voorhees said, fraud, theft, and frauds are all crimes in traditional finance and so should be too in crypto finance. But what if these projects were never allowed to launch due to regulations of who can launch an ICO?

4.5) ICOs and How To Regulate Them

An ICO is an initial coin offering. It is the cryptocurrency version of an initial public offering (IPO) when a business first lists as public and lists its shares on a stock market. Both are a way of raising funds before launching. A major difference is the lack of regulation for an ICO. Many ICOs lead to rug pulls and all funding is pulled out through a backdoor by the project's leaders. It is bubble mania and playing off the hype in many of these instances. At the height of the Netflix series Squid Game's popularity, a squid game coin price rapidly increased before dropping to zero in front of everyone watching on. There is a video out there of a guy streaming as it drops to zero. It is definitely worth a watch to show how quickly these coins can eviscerate people's money.

A slight new variation of an ICO is an IEO. An initial exchange offering works by having an exchange as the middleman. Not very decentralised but adds a layer of security between customers buying and the leaders of these projects as there is more regulation.

One key element of regulation for ICOs comes from countries waiting for others to make regulation decisions and to see how it unfolds. Or existing laws are used. Because the process for raising funding is very different, ICOs require their own regulation. IPOs offer shares in a company. ICOs offer tokens or coins that don't directly represent ownership of the company.

As I've stated, there needs to be regulation to enter the crypto space so fraudsters and scammers can't enter with as much ease and steal customer funds. Of course, as Voorhees said in the interview on Bankless, it is a crime and should be punished as financial crime outside the crypto sector would. But, if we can put deterrents in place to stop the crime from occurring in the first place, we would be on the way to growing trust in the crypto space yet again.

4.6) Who is At Risk Now

Because so many companies are integrated, these bankruptcies will affect most crypto firms and even businesses outside of crypto that have relationships with crypto firms such as through partnership and sponsorship. CeFi is controlling the market narrative currently. But then who knows the difference between DeFi and CeFi? The differences are one of the most vital elements of cryptocurrency and the permissionless, decentralised environment for which they were first created.

A lot of businesses had advertising links with FTX. The home of the Miami Heat basketball team was called the FTX Arena. Mercedes in Formula 1 had FTX plastered all over their car, which has now been removed. Tom Brady endorsed FTX. They advertised everywhere and were incredibly well known. This led to them being more of an institutional exchange versus a retail exchange. An institutional investor is an individual, company or organisation that invests on behalf of clients. A retail investor is a person who invests for themselves.

FTX’s integration into the world we live in, and it's very public bankruptcy, will have effects that spread through the entire industry. Any partnerships will be questioned in the future. For a celebrity to endorse crypto, more payment will be expected to counter the personal risk if something were to go wrong. Look at Kim Kardashian being punished for promoting a cryptocurrency by paying $1.26 million. The reasons for a celebrity or public figure endorsing a crypto coin are dropping rapidly due to a massive increase in distrust of crypto firm practices.

This distrust is felt by everyone. Liquidity in the market is the key driver of crypto prices. This liquidity goes through dry periods known as crypto winters and then when recency bias fades, and crypto gets quiet, it slowly starts building liquidity again and prices soar. The previous cyclical market low is never reached in the next market cycle, or it hasn’t been yet. If crypto has less trust, there will be less money coming in. We thought the crypto winter was upon us months ago. More drying up of liquidity could stretch out and worsen this winter.

On the Odd Lots podcast, guest James Block today discusses how crypto doesn’t create money or value productively. It is an unproductive sector and money flows in from believers in the system. FTX will reduce believers in the entire system. If it’s not worth the risk of incredibly high future returns most retail investors will look elsewhere or maintain their current capital. Especially as fiat inflation rises, people will prioritise protecting themselves and their families by putting food on the table and a roof over their heads. Punts on crypto shitcoins for a 10,000% return will not be at the forefront of most people’s minds, even if it has in the past when everyone threw their free money stimulus checks into assets. We’re paying the price for that now with high inflation.

So what can we look at to see who’s at threat? Look at bankruptcy filings, financial accounts, and who is freezing withdrawals. Look at which companies are audited and who by. A big four accounting firm (KPMG, PWC, Deloitte, EY) would be a good sign that a proper audit has been completed. Proof of reserves and transparency is key. If any crypto firms are this transparent, look at what their reserves are made up of. FTX didn't hold any BTC in their reserves. And Crypto.com have 20% of its reserves in Shiba Inu. It’s like they have a random coin generator and just throw whatever percentage into it that they feel like. Its what I like to call random number generator economics.

5) Concluding Remarks

I’ll conclude by saying what the cryptocurrency market is missing. Knowledge and transparency. Market participants, and clearly the businesses in the space, need to know how to operate safely and sustainably, to build trust again. These companies need to be transparent with their customers, and not forge or falsify financial accounts.

It’s been seen many times. The company comes out and says, “we are pausing withdrawals due to problems regarding liquidity,” but do not worry. The next day, filing for bankruptcy. It could be blamed on the masses, but if they were more knowledgeable, they would only invest in crypto projects that they believe in the long-term future of. Those that can truly disrupt the future of our global financial system. But the responsibility solely lies with the businesses in the space. More thought into how these companies are structured is necessary. The volatility of the crypto market must be considered, and contingencies put in place to manage the most extreme of planned scenarios.

The trust has been severely damaged. And it will take a long time to rebuild. But the first iteration of a new disruptive technology often doesn’t become the face of the industry. Is this the end of the first iteration, and the beginning of the second? I hope so, and I hope the second will change how our financial system works forever, in a way that benefits us all.

References

Bankless on their episode with Matt Walsh said that we need more adults in the crypto space. I don’t think this is true, but I understand what they were getting at. We often see young people bring great innovation and fantastic ideas throughout history with energy and passion. The crypto space just needs fewer scammers, thieves, and in short, pricks. There needs to be some deterrent to others trying something similar to FTX again. They also discussed that FTX Was Not Allowed to Trade in the US But Did. -

https://www.home.saxo/en-gb/content/articles/cryptocurrencies/ta-crypto-collaps-not-over-10112022

https://www.home.saxo/en-gb/content/articles/cryptocurrencies/binance-steps-away-from-ftx--contagion-is-on-the-horizon-10112022

https://www.home.saxo/en-gb/content/articles/cryptocurrencies/contagion-may-follow-08112022

https://www.reuters.com/technology/binance-halts-ftt-deposits-ceo-says-2022-11-13/

https://www.zerohedge.com/markets/convicted-elizabeth-holmes-pleads-lenient-18-month-sentence-home

https://www.zerohedge.com/political/ftx-founder-spent-40-million-democrat-midterm-megadonor

https://www.zerohedge.com/markets/ftx-held-just-900mm-liquid-assets-vs-9bn-liabilities-video-emerges-confirming-alameda-knew

https://www.zerohedge.com/crypto/binance-dominates-crypto-exchange-landscape

https://www.benzinga.com/markets/cryptocurrency/22/11/29690823/20-of-crypto-com-reserves-are-on-this-meme-coin

https://www.benzinga.com/markets/cryptocurrency/22/11/29690125/thats-what-ended-up-breaking-it-vitalik-buterin-tells-benzinga-what-broke-ftx-why-solana-e - Solana Impact

https://www.benzinga.com/markets/cryptocurrency/22/11/29690443/musk-declares-doge-to-the-moon-and-the-meme-crypto-takes-off

https://www.cnbc.com/2022/11/12/sam-bankman-fried-reportedly-denies-fleeing-to-argentina-says-hes-still-in-the-bahamas.html

https://www.cnbc.com/2022/11/12/ftx-says-its-removing-trading-and-withdrawals-moving-digital-assets-to-a-cold-wallet-after-a-477-million-suspected-hack.html

https://uk.finance.yahoo.com/news/f-d-rise-fall-us-160443752.html

https://uk.finance.yahoo.com/news/elizabeth-holmes-prosecutors-seek-15-173323635.html

https://uk.finance.yahoo.com/news/hacking-fears-650m-vanishes-collapsed-200000541.html

https://uk.finance.yahoo.com/news/least-1bn-investor-assets-missing-200035177.html

https://www.ft.com/content/c6658ce8-26a3-4580-9e64-6083a7d35eca

https://www.ft.com/content/79b6f14c-110a-4c66-82e2-286003c34717

SBF and Erik Vorhees Video -

https://www.ft.com/content/0fa4f3b6-213c-4e76-bcd9-fcf184a264a2

https://www.ft.com/content/afe56c4e-2d68-457e-bbb2-476752d5f02e

https://www.ft.com/content/dc08ed9f-0f3b-45fb-a5f6-b87157fdf944

https://www.ft.com/content/726277bb-35a1-4d35-9df9-3e1cca587b77

https://www.ft.com/content/67b1899f-4b1f-4676-b264-0d19e205d64e

https://www.ft.com/content/f05fe9f8-ca0a-48d5-8ef2-7a4d813af558

https://geopolitics.co/2022/11/13/billions-of-usd-laundered-as-aid-to-ukraine-laundered-back-to-democrats-via-ftx-crypto-platform/

https://www.ft.com/content/ad84e038-37b5-4612-a8d6-c9bf8363f456

https://www.ft.com/content/00105bdd-ab13-4416-b504-ce22bfe7b589 - CZ

https://www.cnbc.com/2022/11/14/cryptocom-ceo-says-will-prove-naysayers-wrong-amid-ftx-contagion-fears.html

https://www.benzinga.com/markets/cryptocurrency/22/11/29694101/binance-ethereum-dogecoin-rebound-after-binances-cz-declares-industry-recovery-funds-to-ea

https://www.fnlondon.com/articles/ftx-binance-liquidity-crypto-crisis-hedge-funds-exchanges-20221109?mod=home-page\&adobe_mc=MCMID\%3D42224388335492773619219513970315532381\%7CMCORGID\%3DCB68E4BA55144CAA0A4C98A5\%2540AdobeOrg\%7CTS\%3D1668445377

https://www.marketwatch.com/story/what-h-sam-bankman-frieds-latest-tweets-spark-scorn-as-well-as-concern-11668416557?mod=home-page

https://www.zerohedge.com/political/ftx-founder-sam-bankman-fried-lists-bahamas-penthouse-40-million

https://www.zerohedge.com/markets/manhattan-us-attorney-office-probing-ftx-collapse

https://www.zerohedge.com/crypto/reduce-cascading-negative-effects-ftx-binance-ceo-declares-industry-recovery-fund-support

https://www.zerohedge.com/markets/sbf-questioned-bahamas-police-elon-counters-there-will-be-no-investigation-major-democrat

https://www.zerohedge.com/crypto/ftx-isnt-canary-coal-mine-ftx-coal-mine-it-just-collapsed

https://www.zerohedge.com/markets/hints-many-crises-lehman-enron-mf-global-no-lender-last-resort-banking-late-1800s

https://www.reuters.com/technology/cryptoverse-so-long-solana-ether-rival-clobbered-by-ftx-crash-2022-11-15/

https://www.reuters.com/technology/ftx-officials-contact-with-us-regulators-filing-2022-11-15/

https://advisoranalyst.com/2022/11/13/midterm-outcome-and-ftxs-demise-an-unexpected-turn-of-events.html/

https://www.zerohedge.com/crypto/ceo-ukrainian-crypto-firm-denies-ftx-ukraine-money-laundering-allegations

https://www.marketwatch.com/story/bitcoin-in-your-401-k-senators-intensify-pressure-on-fidelity-to-reconsider-crypto-in-retirement-plans-11669073011?mod=home-page – Fidelity

https://www.cnbc.com/2022/11/22/bitcoin-btc-hits-2-year-low-as-ftx-collapse-contagion-fears-linger.html

https://cryptonews.com/news/mastercard-citigroup-other-global-banking-giants-start-digital-dollar-pilot-with-new-york-federal-reserve.htm

https://www.thecoinrepublic.com/2022/11/17/new-york-fed-bringing-cbdc-pilot-mastercard-and-citigroup-to-join/

Genesis - https://www.reuters.com/technology/crypto-lender-genesis-says-no-plans-file-bankruptcy-imminently-2022-11-21/

https://pacer-documents.s3.amazonaws.com/33/188450/042020648197.pdf - Bankruptcy Declaration

Crypto Run vs Banking Run - http://www.bondeconomics.com/2022/11/crypto-failures-versus-bank-failures.html - Occur first in wholesale markets and is usually over when customer rush to ATMs. Gives banks time to act.

https://deadline.com/2022/11/ftx-sam-bankman-fried-movie-michael-lewis-auction-the-dish-1235175725/

https://www.ft.com/content/08370364-40af-4a1c-a85e-a9243be173c8

https://www.ledgerinsights.com/ftx-ceo-flabbergasted-sbf-borrowed-1-billion-from-alameda/

https://hackernoon.com/alameda-loaned-1-billion-to-sam-bankman-fried-and-23-billion-to-paper-bird-inc-aka-sbf-also

https://www.ftxpolicy.com/posts/possible-digital-asset-industry-standards = SBF Paper

https://www.moneyandstate.com/blog/response-to-sbf - Voorhees Response

https://www.nytimes.com/2022/11/18/business/ftx-alameda-ties.html\#:~:text=Alameda\%20Research\%20was\%20Sam\%20Bankman,to\%20help\%20Alameda's\%20trading\%20business.

https://www.investopedia.com/ftx-exchange-5200842

nytimes.com/2022/11/18/business/ftx-alameda-ties.html#:~:text=Alameda%20Research%20was%20Sam%20Bankman,to%20help%20Alameda's%20trading%20business.

https://www.bbc.co.uk/news/world-us-canada-63685131

https://wirexapp.com/blog/post/whats-the-difference-between-an-ico-ipo-ieo-and-sto-0499

https://www.europarl.europa.eu/RegData/etudes/BRIE/2021/696167/EPRS_BRI(2021)696167_EN.pdf

https://cointelegraph.com/news/3ac-a-10b-hedge-fund-gone-bust-with-founders-on-the-run

https://www.foxbusiness.com/politics/ftx-founder-sam-bankman-fried-prolific-donor-republicans